We widely agree that a single fuel cannot lead the UK to net zero. As electrification dominates the debate on heat of decarbonization, here is the argument from Orlando Minervino, lead Xoserve’s decarbonization strategy: Is the UK overlooking biomethane as a potential solution?

DNV’s 2025 UK energy transition outlook warned that the UK may not meet its net zero target by 2050 due to a lack of clear plans for decarbonized buildings.

No final decision has been made on domestic thermal decarbonization, but full electrification faces major challenges, particularly in grid capacity.

The UK is working towards a transition to the 23 million homes that currently rely on gas heating, addressing the challenges of expanding their electricity infrastructure.

In this context, given the risks that have not reached legally binding targets, shouldn’t energy transition leaders thoroughly investigate all fuel sources and maximize the potential of short- and long-term solutions?

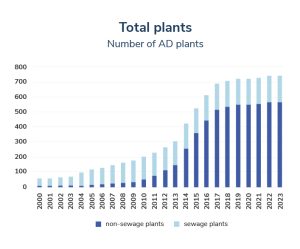

Biomethane is a rapidly growing renewable energy source, with over 700 biomethane plants in the UK alone, doubled over the past decade. In the European Union, France is one of the leading countries in expanding biomethane production, almost doubled its capacity since 2022.

Good natural gas twins

By removing impurities such as carbon dioxide, water, and hydrogen, biomethane becomes chemically identical to methane found in natural gas. However, it is made not from fossil fuels, but from organic materials such as food waste, agricultural residues, or sewage that decomposes in the absence of oxygen. This is a process known as anaerobic digestion.

Biomethane has a high methane content (usually 95-99%), making it ideal for any application that uses natural gas, such as heating. Biomethanes could play a key role in achieving the zero-zero target, as they emit significantly lower greenhouse gases than fossil fuels.

One of the advantages of biomethane is that it can be injected directly into existing gas grids without the need for expensive infrastructure upgrades. Data from the Anaerobic Digestion & Bioresources Association (ABDA) show that there are currently 141 injection plants in the UK. Biomethane is also easy to store, providing more consistent production volumes compared to renewable sources such as solar and wind power. This predictability helps effectively balance the balance between energy supply and demand.

Additionally, this gas may be carbon negative. For example, if organic matter comes from food waste or fertilizers, these materials decompose over time and release methane into the atmosphere. Instead of escaping this methane, biomethane production captures it and makes effective use of it, preventing harmful gases from being released into the atmosphere.

It can also be produced from other readily available waste such as agricultural waste and wastewater, creating a circular economy that complements the waste sector.

That’s not that biomethane doesn’t release any carbon emissions at all. Biomethane production and upgrades require energy from fossil fuels, which could contribute to overall carbon emissions.

Currently, this situation is similar to other energy generation processes. For example, 38.3% of UK power generation comes from fossil fuels. However, biomethane production may use surplus renewable energy in the future.

Building blocks in the biomethane market

Realizing the full potential of Biomethane requires a clear and consistent policy framework that drives investment and growth. The policy environment surrounding biomethane is a complex picture of progress and gaps. There have been a lot of positive developments, but there is a need for more clarity and a more strategic direction.

Currently, biomethane has two government support schemes. Green Gas Support Scheme (GGSS) and Green Gas Collection (GGL). GGSS is a government scheme designed to encourage the production of biomethane for injection into gas networks by providing payments to biomethane producers of all units of biomethane injected. GGL supports GGSS by imposing obligations on gas suppliers to fund schemes that include payments for quarterly collections.

In 2023, GGSS was extended until March 2028. This is a big win for the industry as it drives production and makes biomethane a more financially viable proposal. By offsetting the high initial investment costs associated with anaerobic digestion plants and biogas upgrades, biomethane becomes a competitive fuel to produce.

Still, other opportunities have been overlooked. For example, Energy Security and Net Zero’s December Clean Energy Action Plan acknowledged the possibility of biomethane generating and gas decarbonization, but there were no specific plans for integration into the gas network.

By 2050, it is estimated that annual power generation will reach 692 TWH. The government’s biomass strategy shows that producing about 30-40 TWH of biomethane by 2050 will contribute to the UK’s goal of achieving net zero emissions, accounting for just 5% of total generation. However, this number is too modest, with biomethane targets reaching up to three times more achievable.

The national biomethane strategy and roadmap will provide producers, investors and developers with long-term plans and will help clarify how fuel should be used in different sectors over the next few years. It also allows you to establish clear production targets and outline grid integration plans.

Additional consultations with energy leaders are important to promote market development and further reduce heating emissions. These need to explore mechanisms that can promote biomethane fusion into natural gas networks.

Additional consultations with energy leaders are essential to drive market development and further reduce heating emissions. These discussions need to explore mechanisms that promote biomethane fusion into natural gas networks, including the potential implementation of gas blend mandates that require a set percentage of biomethane injections.

Equally important is to streamline the planning and permitting processes for non-abel digestion plants and biomethane upgrade facilities, allowing faster project deployments across the UK. However, this challenge is not inherent to biomethane, but it is widely applied to all renewable energy technologies.

Drawing resourceful routes

Contrary to the UK’s ambitious emissions targets and the undeniable challenges of a fully electrified strategy for heating, biomethane stands out as an essential energy source that no longer overlooks.

As a “good twin” to natural gas, biomethane provides a resourceful route to using existing infrastructure and raw materials. Its production not only significantly reduced greenhouse gas emissions from building heating, but also helped to divert waste from landfills, contributing to the circular economy.

Despite the rapid growth of the biomethane industry across the UK and Europe, its immeasurable potential is largely underestimated. The current government incentives are a step in the right direction, but more can be achieved. A comprehensive biomethane strategy is essential. This includes establishing a robust market with mechanisms such as ambitious production targets, seamless integration into gas grids, and gas blend mandates and streamlined permitting processes.

To achieve a fully decarbonized energy system, the UK must pursue a diverse approach. Biomethane is more than just a complementary fuel. This is a scalable and environmentally beneficial solution that can play a key role in future energy mixes.

Maximizing the possibilities of all viable energy sources is essential for a successful clean energy transition.

Source link